The one thing we know will never stop is constant change. I watched the transition from boxed software to the cloud happen firsthand. I remember when you bought a CD-ROM, installed it on your machine, and that was clearly a product. Then came SaaS (Software as a Service), and the same tool became a monthly subscription.

Technology swallowed the difference between owning and using. But not everything evolved at that pace. Our tax legislation stayed frozen in time, trying to fit the new economy into old boxes. "Is this a product or a service?" accountants would ask. "Whose tax is it, the state's or the municipality's?" auditors would argue.

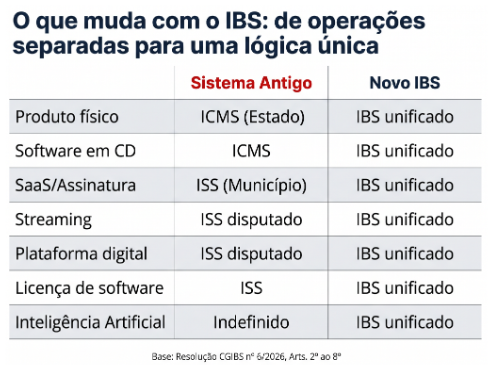

Well, that fight is finally over. At least, it will be, and that is what Resolução CGIBS nº 6, of April 30, 2026, which regulates the Imposto sobre Bens e Serviços (IBS), establishes.

I have always taken a pragmatic approach to regulations. Legal jargon does not interest me. What interests me is how a rule changes the game in practice. And the change here is structural. The tax reform, embodied in Articles 2 through 8 of the new resolution, creates a single logic. The schizophrenia of taxing a physical product, software, streaming, or an Artificial Intelligence platform differently is over.

The rule is now straightforward: the IBS applies to onerous transactions involving goods or services. And the concept of "good" has been stretched to its limit. Tangible goods, intangible goods, rights, and economically valuable assets. Everything is in the same bucket. If you deliver, make available, license, assign, or grant, you are performing a "supply" of a good.

It seems that being a "good" citizen will now mean being a taxable one (I could not resist the pun).

For anyone operating digital businesses, marketplaces, or holding structures, this is an earthquake. Think of a hybrid model where you sell hardware bundled with an AI software subscription. Before, you had to split the invoice, separate ICMS from ISS, deal with two bureaucracies and two credit logics. Now, the resolution states clearly that when there is a primary supply with ancillary components, everything follows the treatment of the primary element. If no clear hierarchy exists, the rule is to unify the tax treatment, unless the treatments are explicitly distinct.

Do not be misled into thinking life simply got easier. It got more monitored. The resolution closes in on aggressive tax planning. Article 5 makes it clear that non-onerous supplies, or those below market value, to related parties are also subject to tax. That is right. What about that asset transfer between companies within the same group at an understated value? Or that expensive gift given to a partner? The tax authority now has the power to set the market value and charge IBS on that basis.

As I said, technology swallowed the bureaucracy, and the bureaucracy, predictably, responded by building a much wider capture net. What is still not entirely clear to me, though, is how the tax authority will, in day-to-day operations, distinguish the "ancillary service" from the "primary" one in complex technology contracts. The definitive criteria for electronic valuation still depend on future joint acts from the Receita Federal and the Comitê Gestor do IBS.

The digital revolution already erased the line between product and service in the consumer's mind. The government just needed to catch up. Now it has. And it will send the bill. The question for business owners is no longer "which tax do I pay?" but rather "how do I restructure my contracts and business model for this new reality?"

If you think this is too complex, or that some major reversal will come along and change everything, there is one thing to be said: passivity will be costly. Those who do not understand the new rules of the game will lose margin and competitiveness very quickly. We have already seen that happen in far smaller tax shifts. Imagine what it will look like in a transformation this sweeping. It will hurt whoever is not prepared.

Article originally published on GazzConecta.